World Gold Council Gold Demand Trends: 2014 Full Year Report

2014 ends with strong gold demand in Q4, driven by jewellery and central banks

2014 saw a stabilisation of the gold market as it pulled back from the extremes of 2013, according to the latest Gold Demand Trends full year report from the World Gold Council. Annual gold demand was 3,924 tonnes (t), 4% lower than 2013. The year ended strongly, with gold demand in Q4 2014 up 6% year on year to 987t, driven by demand for jewellery and central bank buying.

Jewellery remains the biggest source of demand for gold. Total jewellery demand for the year was 2,153t, down 10% compared to the previous year, which is not surprising given the price-driven jewellery demand surge in 2013. India – one of the two largest gold markets in the world – had its strongest year for jewellery demand since the World Gold Council’s records began in 1995, up 8% on a year ago to 662t. This was driven by wedding and festival buying despite the presence of government restrictions on gold imports for most of the year. Although China saw demand decline 33% year on year, it still represents the second best year for jewellery demand in China since our records began.

Investment demand, the other big driver of the gold market, was up 2% in 2014, from 885t in 2013 to 905t last year. Total bar and coin investment was down 40% as investors who had made major purchases in 2013 held back from further purchases. This was offset by a dramatic slowdown in outflows from exchange traded funds (ETFs), from 880t in 2013 to 159t in 2014.

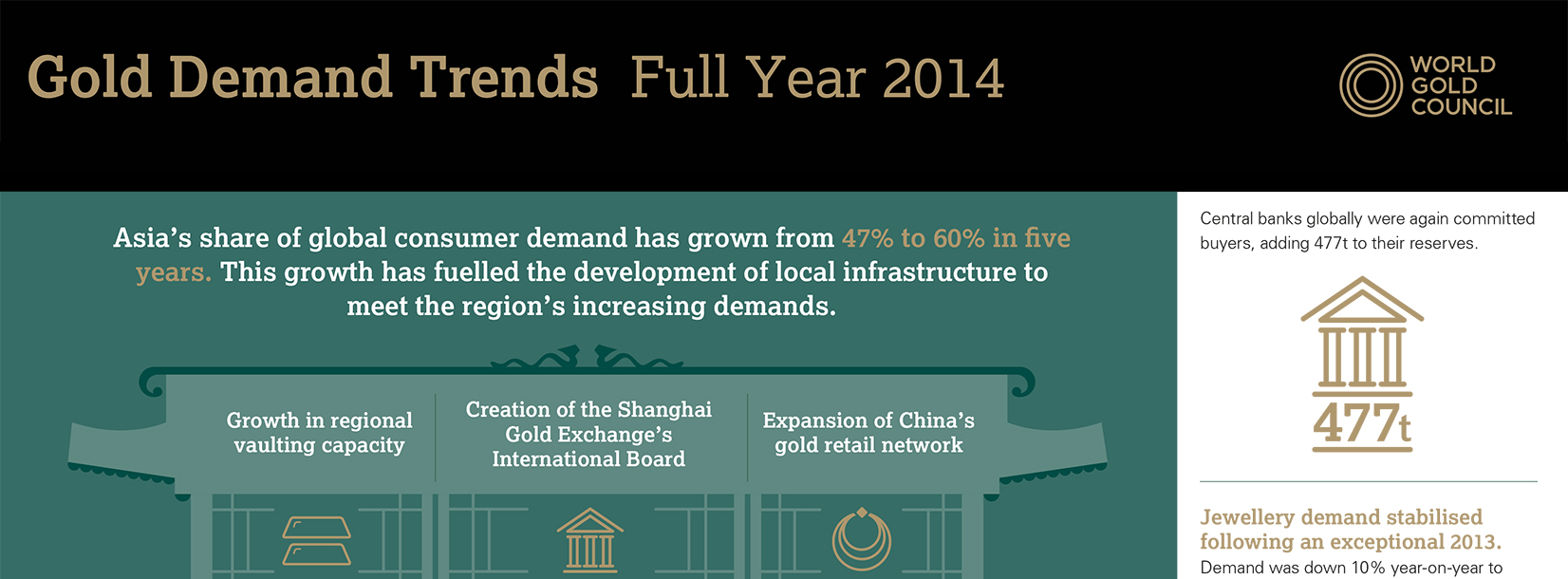

Central banks continued to see the value of gold as a reserve asset in 2014. Annual central bank demand was up 17% to 477t. This was particularly evident in the last quarter of 2014, when demand was up 40% year on year to 119t, making Q4 2014 the 16th consecutive quarter and 2014, the fifth consecutive year that central banks were net purchasers of gold.

Total supply in 2014 was virtually unchanged compared to 2013 at 4,278t, as recycling contracted to a seven year low, offsetting annual mine production growth, which was up 2% to a record 3,114t.

Marcus Grubb, Managing Director, Investment Strategy at the World Gold Council commented:

“2014 was a year of stabilisation and innovation in the gold market, with annual gold demand down by just 4% after the record-breaking level of buying seen in 2013. It was a standout year for Indian jewellery, despite government restrictions on gold imports, reinforcing the nation’s affinity with gold. Meanwhile Chinese gold demand returned to those last seen in 2011/2012 as consumers and investors took time to digest the substantial volumes accumulated in 2013.

“What’s particularly notable about 2014 is that the striking shift in physical gold demand from West to East is now being followed by gold infrastructure development in Asia. New products and trading platforms were introduced like the Shanghai Gold Exchange International Board,

the “Gold Send” mobile app in Turkey and the new kilobar contracts in Singapore and Hong Kong - all designed to make gold more accessible to greater numbers of buyers in the East.”

The key findings of the report are as follows:

-Following an exceptional 2013, gold demand stabilised in 2014, declining just 4% to 3,924t.

-Jewellery remains the biggest component of demand for gold. Indian demand for jewellery was up 8% to 662t, the best year of jewellery demand since records began in 1995 and China’s jewellery demand whilst down 33% was still the second best on record.

-There was also strong jewellery demand in the UK and US, driven by improved economic performance, up 18% to 28t and 9% to 132t respectively.

-However, overall jewellery demand fell by10% to 2,153t as China digested the record breaking levels of jewellery accumulated in 2013.

-Annual central bank demand was up 17% to 477t, the fifth consecutive year and 16th consecutive quarter that banks were net purchasers of gold.

-Investment was up 2% to 905t last year, despite a fall of 40% in bar and coin investment to 1,064t as consumers who purchased in 2013 held back from further buying. ETF outflows slowed significantly, from 880t in 2013 to 159t in 2014.

-Total supply in 2014 was virtually unchanged compared to 2013 at 4,278t. Recycling contracted to a seven year low, down 11% to 1,122t. This offset the increase in annual mine production, up 2% to a record 3,114t - a level that we expect will signal a plateau over 2015. Additional gold demand and supply statistics for Full Year and Q4 2014

-Global demand for jewellery was 2,153t for the year, down 10% on 2013. Q4 global jewellery demand was 575t up 1% from Q4 2013.

-Fourth quarter gold demand of 987t was up 6% versus Q4 2013.

-Investment demand was 905t up 2% on 2013, with a 40% drop in bar and coindemand to 1,064t. The quarterly figure was up 10% to 198t.

-ETF outflows slowed for the full year from 880t in 2013 to 159t in 2014.

-Full year demand in the technology sector was 389t, down 5% on 2013. Technology for Q4 saw modest declines, totalling 95t, down 3% year on year.

-Total supply for the year was 4,278t, virtually unchanged compared to 2013. The quarterly picture saw total supply at 1,091t, down 2% on Q4 2013.

-Net central bank purchases totalled 119t for Q4 up 40% on Q4 2013.

The Full Year 2014 Gold Demand Trends report can be viewed here.

Sorry, you must be logged in to post a comment.