World Gold Council Gold Demand Trends Q2 2014

From gold.org:

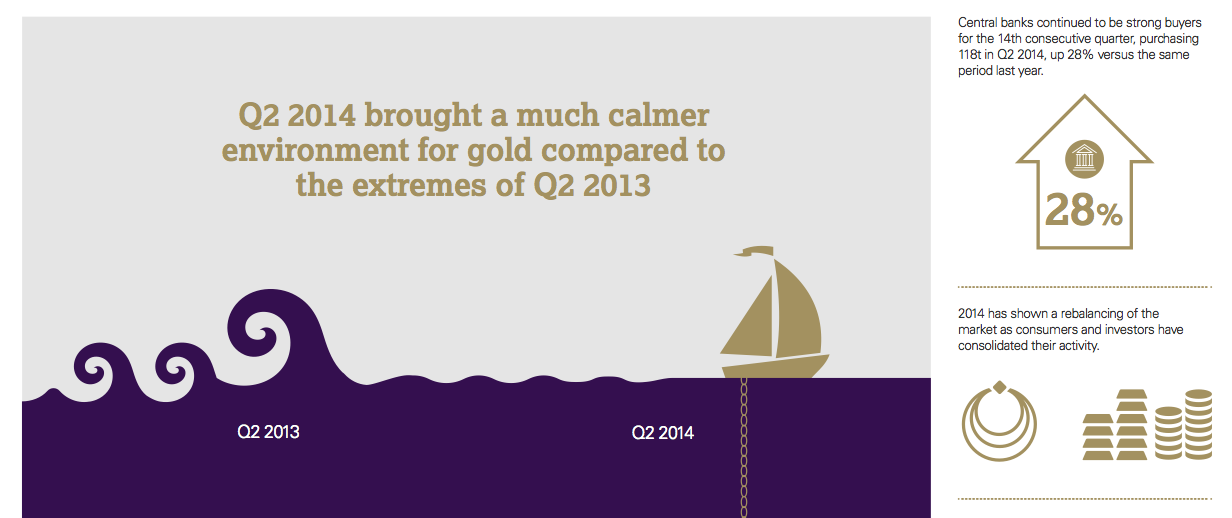

Gold demand of 964t in the second quarter was, unsurprisingly, lower when compared with the exceptional upsurge in demand in Q2 2013. Jewellery demand weakened year-on-year, but the broad, 5-year uptrend remains intact. Investment demand pulled back from the extremes seen during last year as relatively stable price conditions contributed to the subdued environment. Central banks continued to buy gold at a solid, steady pace. Mine production grew 4% year-on-year for a second consecutive quarter, contributing to a 10% increase in gold supply.

In value terms, gold demand in Q2 2014 was US$40bn, down 24% compared to Q2 2013. The average gold price of US$1,288/oz was down 9% on the average Q2 2013 price.

The key findings from the report are as follows:

-Jewellery remains the biggest component of gold demand, representing more than half of all demand at 510t. Although it is down 30% year on year, jewellery has been extending the broad upward trend from the base established in early 2009.

-Central banks increased purchasing by 28% to 118t compared with the same period last year, as they continued to use gold as a hedge against risk and diversify away from the US dollar.

-Total investment demand (combined investment in bars and coins and ETFs) was up 4% to 235t. However, there was a 56% decrease in bar and coin demand from 628t in Q2 2013 to 275t in Q2 2014 following unprecedented levels of demand last year.

-ETF outflows were 40t, a tenth of the outflows seen in the same period last year

-Taken together, these factors show that gold demand is reverting to long term trends after an extraordinary 2013.

-Total supply for the quarter was up 10% year on year solely due to the growth in mine supply.

-H1 recycling is the lowest since 2007 although the figures for Q2 2014 are up 1% to 263t compared to last year - a relatively low figure compared to the historical average.

-Gold demand and supply statistics for Q2 2014

-Gold demand for Q2 2014 was 964t, down 16% year on year from 1,148t

-Central bank purchases rose 28% year on year, to 118t from 92t

-Total bar and coin demand fell by 56% year on year, to 275t from 628t

-ETF outflows were 40t, a tenth of the outflows seen in the same period last year

-Total jewellery demand fell by 30% year on year, to 510t from 727t

-Technology demand came in at 101t, down 3% versus the same period last year

-Total supply increased by 10% to 1,078t. We expect supply to peak in 2014 and plateau over the next 4-6 quarters.

Sorry, you must be logged in to post a comment.